Aerodrome: Taking Flight

Every chain eventually has a few dominant exchanges. But uniquely for Base, that exchange is Aerodrome.

The question worth asking isn't whether Aerodrome is a good protocol. It clearly is. Instead it's whether its tokenomics, which work beautifully as a near-monopoly on one chain, will still work on other, more competitive chains.

Soon we'll find out. Aerodrome's merger with Velodrome, the move to Ethereum L1, and its MetaDEX 03 upgrade — will turn it from a single-chain dominator into one competitor among many. Base was the incubator where the model works, now Mainnet is the real test.

Let's review whether the lock-to-emission equilibrium that makes the token work can survive on a chain where Aerodrome is no longer the only game in town.

The Base-ics

You cannot look at Aerodrome without first addressing Base. The two are not separable today, and they won't be fully separable after Mainnet launch. If activity on Base contracts, Aerodrome's revenue base contracts with it.

So what does the Base picture look like?

Base is by far the strongest L2. It captured the majority of total L2 revenue in 2025, and its TVL climbed from $3.1 billion in January 2025 to a peak above $5.4 billion in October. As of mid-April 2026, following its OP integration, TVL has crossed $4.5 billion again and trending upward.

The structural advantage here is Coinbase's strong distribution. With millions of monthly active trading users and over 110 million verified accounts, Coinbase doesn't need to bribe users onto its chain. The Coinbase-Morpho lending integration showed this clearly: $866 million in loan applications flowing through Morpho on Base. Many of those users might not even realize they're using DeFi — users never chose Base, Coinbase chose Base for them.

The Aerodrome-Coinbase relationship runs deeper than distribution too. Coinbase Ventures is itself an active veAERO voter. The Base Ecosystem Fund has directed emissions toward pools Coinbase wants deepened, starting with cbBTC. Animoca joined as a governance participant in late 2025, locking their own AERO.

Base App extends the funnel further. In-app swaps route to whatever has the deepest liquidity on Base, which in practice is frequently Aerodrome.

The result is a vertically integrated stack. Coinbase provides the app. Base provides the chain. Aerodrome provides the liquidity. CB Ventures sits inside Aerodrome's governance making sure capital ends up where Coinbase wants it. Aerodrome's top pools have at times surpassed Coinbase's exchange on volume for specific pairs.

Two structural risks remain though. First and most obvious is concentration: Base is a single-sequencer chain run by Coinbase, and the decentralization roadmap hasn't been fully executed. Second, repricing: if Ethereum raises costs or tightens the economic terms L2s depend on, the economics of every protocol on Base change.

Neither risk seems imminent, and both stand to diminish as Aerodrome expands beyond Base.

What Aerodrome Actually Is

@AerodromeFi launched in August 2023 as a fork of @VelodromeFi on @Optimism, adapted for @base. Both protocols share the same dev team at @DromosLabs.

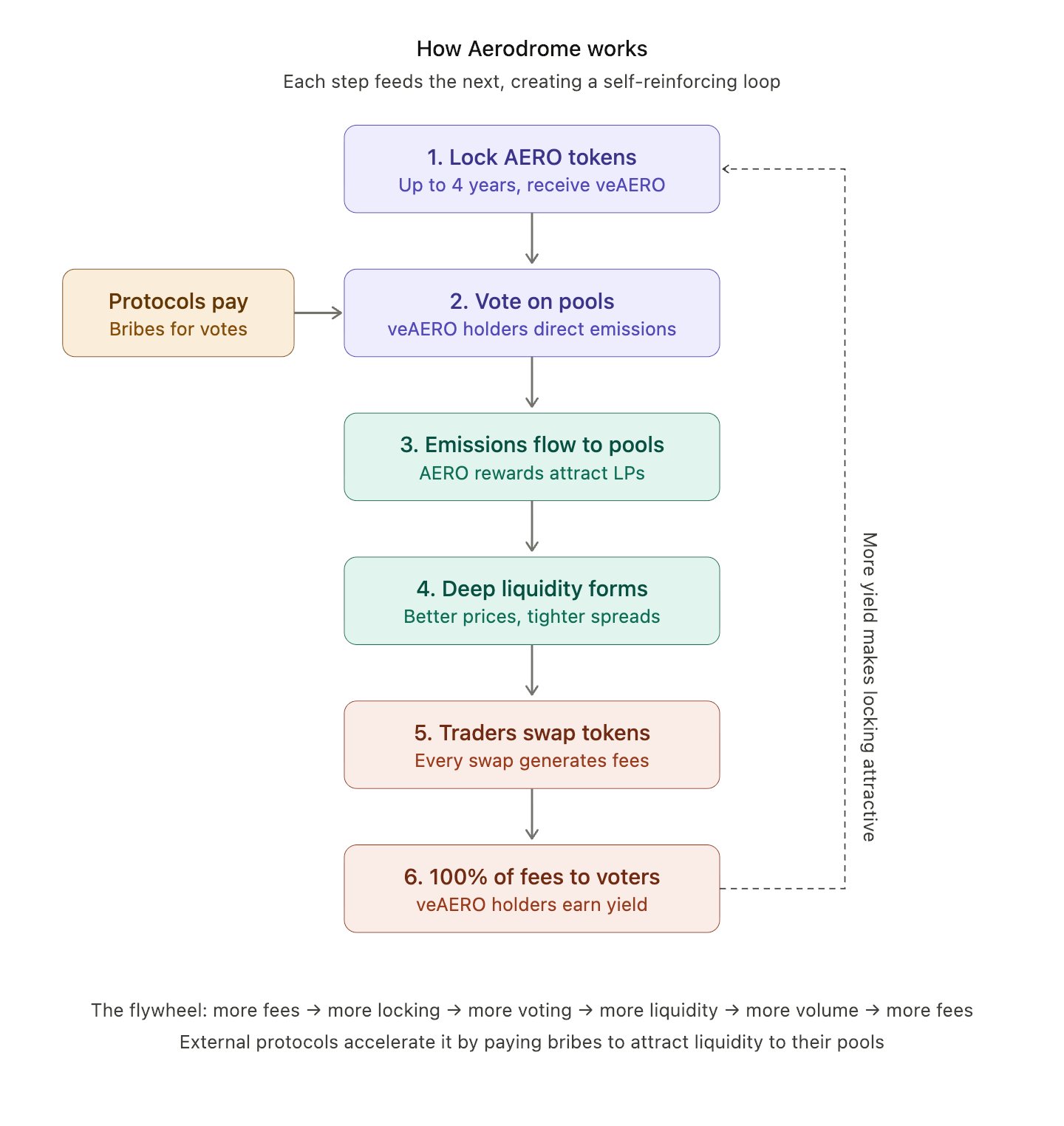

Its core mechanism is a vote-escrowed (ve) AMM. AERO can be locked for up to four years to receive veAERO, a governance position that grants two things: voting power over where weekly emissions go, and 100% of the trading fees from the pools the holder votes for.

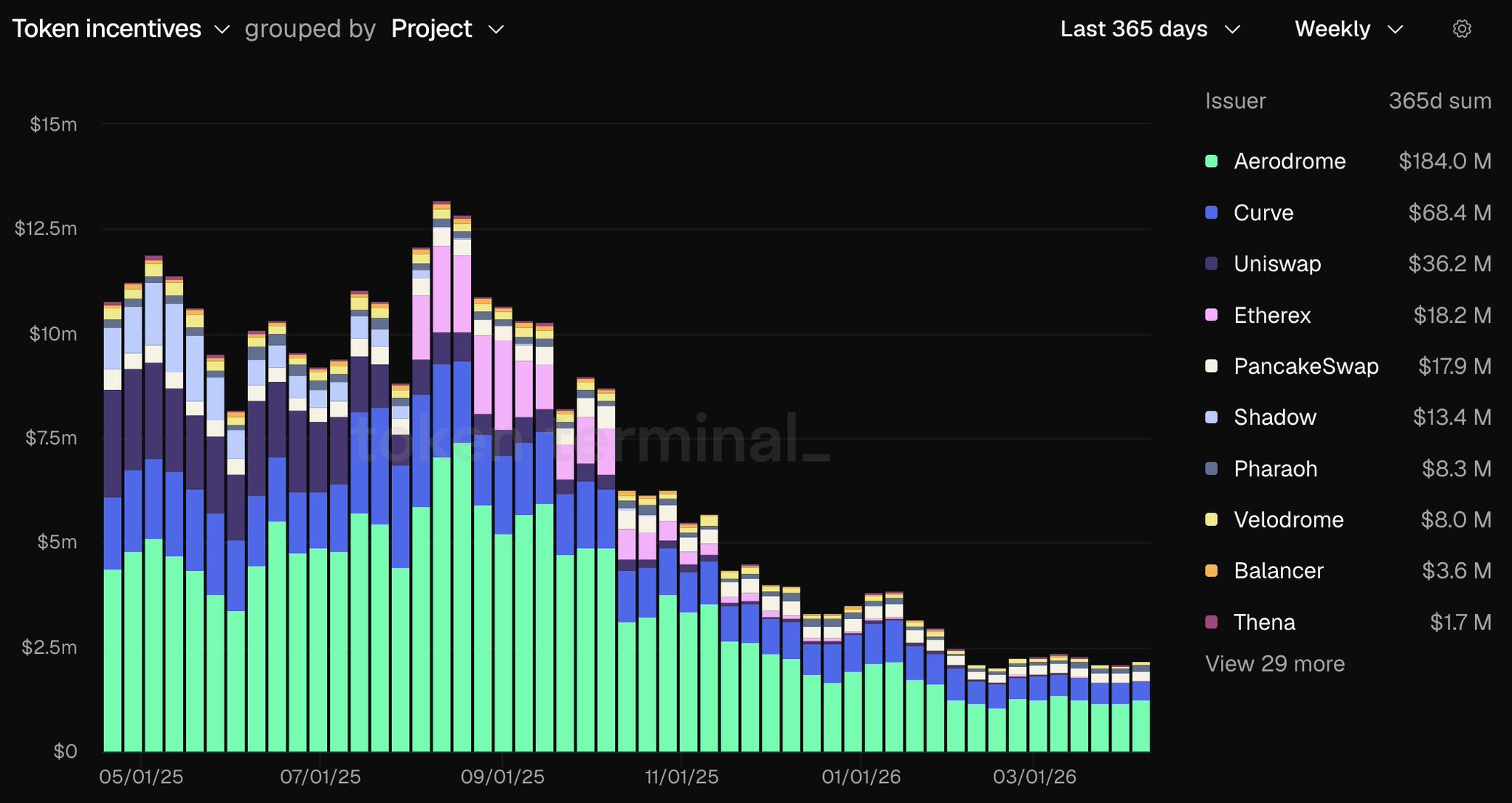

The design creates a flywheel. Protocols that want deep liquidity pay "bribes" to veAERO holders to direct emissions toward their pools. Emissions attract LPs, which tightens spreads, which attracts volume, which generates fees, which makes veAERO more valuable, which attracts more locking. On and on.

What Curve pioneered, Velodrome refined — and Aerodrome executed it the right chain at the right time.

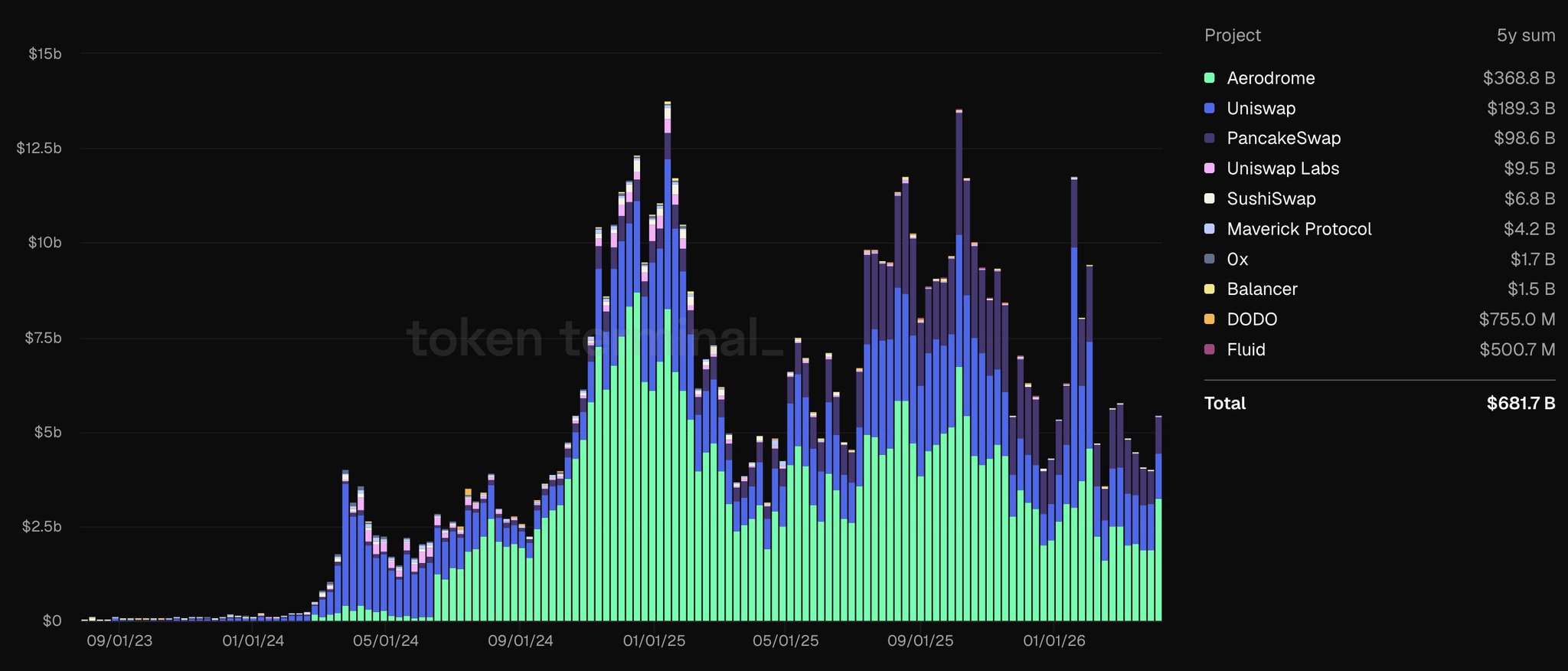

On Base, the results have been decisive. Aerodrome controls over half of the Base DEX volume, 43% of all Base application revenue ($160.5M of $369.9M in 2025), and supports 100+ protocols on the chain.

When Coinbase launched cbBTC, Aerodrome's cbBTC volumes flipped wrapped Bitcoin on Ethereum mainnet after one week. When Mezo, a Bitcoin-native lending protocol, needed to bootstrap liquidity on Base, it streamed 2.25% of its token supply to veAERO voters.

If you launch a token on Base and you need liquidity, you're likely to use Aerodrome.

Value Accrual During Rough Times

AERO has perfect token value accrual. No team unlocks, no investor unlocks. Every dollar of fees flows directly to veAERO holders, which means any test of the Aerodrome model shows up cleanly in numbers.

That test came in Q4 2025 when AERO slid 60% from its highs. Broader DeFi was bleeding activity, and this was the type of environment where revenue-subsidized tokenomics typically break. Fees fall faster than emissions and locks unwind.

Aerodrome did the opposite. In September 2025, monthly protocol revenue exceeded emissions for the first time. The pattern has held through Q1 2026. In recent weeks, more AERO has been locked than emitted, curbing supply.

Aerodrome's equilibrium in a drawdown is the major signal that separates a working design from one that only functions in a bull market.

The Emission Mission

So how does the equilibrium actually hold?

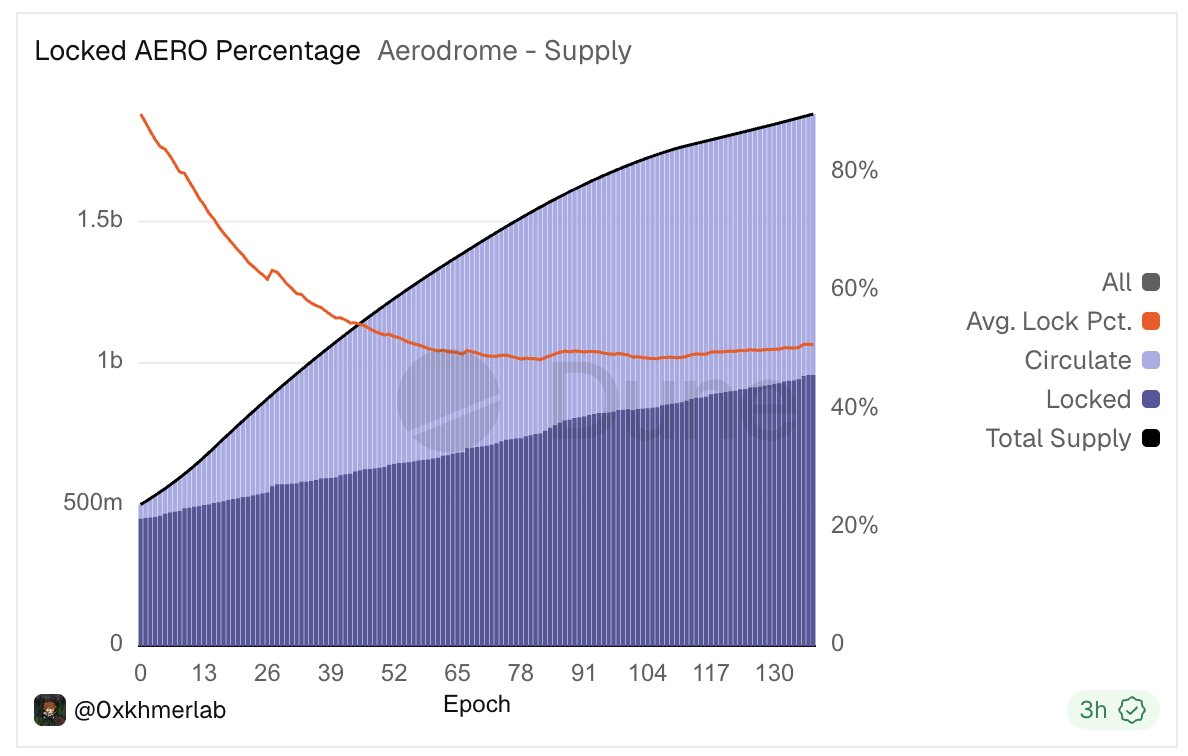

AERO has technically infinite supply. Annualized inflation runs at around 11% but continues to shrink. Circulating supply sits at roughly 922 million tokens against a total approaching 1.88 billion. That's 50% of the supply locked, an average lock duration of around 3.7 years, and most positions clustered near the four-year max.

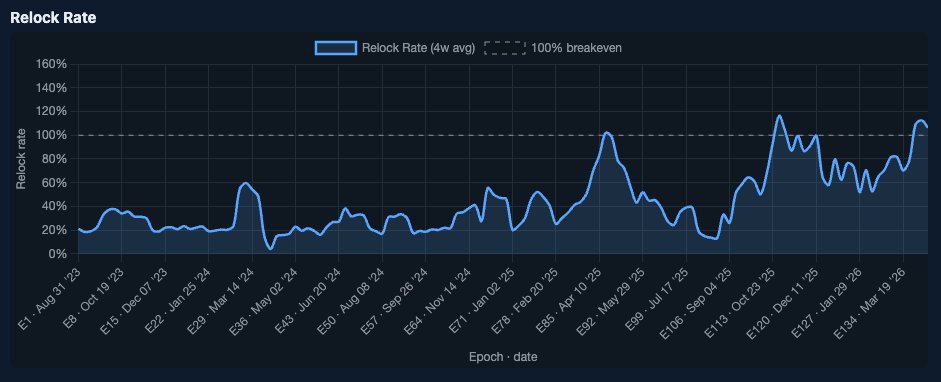

But the number to watch isn't the 50% locked figure. The real measurement is how much new AERO gets locked versus emitted each week. When locks exceed emissions, tradable supply shrinks. When emissions exceed locks, tradable supply grows. This is the Relock Rate, and it tells you whether the flywheel is working.

Average weekly locked AERO growth relative to emissions has recently flipped above 100% recently, trending higher. In fact, 8 out of 13 deflationary weeks have occurred in the last 6 months. Smoothed into 4-week averages, the trend towards 100% is clearer:

This has been due to the adoption of the "Aero Fed" when, on October 9th, Aerodrome fully handed its monetary policy over to veAERO holders. Each epoch (week), voters nudge emissions up or down, letting the protocol react to market conditions rather than follow a fixed decay curve. The result is a reactive equilibrium where voters curb supply to just barely meet locking demand.

This equilibrium gives AERO one of the cleanest value accrual mechanisms in DeFi, and it means the only thing Aerodrome actually needs to do is grow durable volume. Which is exactly what the expansion is supposed to deliver.

The Expansion Experiment

The upcoming merger consolidates AERO and VELO into a single AERO token. 94.5% of supply goes to current AERO holders, 5.5% to VELO holders, mirroring each protocol's revenue share. Importantly, the event will bear no dilution and no new token creation.

MetaDEX 03 introduces a dual-engine architecture. The REV (Revenue) Engine, anchored by Slipstream V3, captures MEV revenue currently leaking to sequencers (Dromos projects a 40% revenue uplift). The AER (Adaptive Emissions Rate) Engine aims to reduce emissions by approximately 25%, equating to around $34 million in annual savings per the Dromos CFO. The team frames the whole thing as connecting to over $80 billion in global TVL, up from roughly $5 billion in combined ecosystem TVL today.

On the L1, Aerodrome will be tested because deep markets already exist for every major pair. A protocol launching on Ethereum doesn't need to bribe Aero voters for an ETH/USDC pool, because that pool already has billions in liquidity elsewhere. Therefore, the bribe economy naturally shrinks to the margins: new token launches, niche pairs, long-tail assets.

PancakeSwap serves as a cautionary tale. It cut daily emissions roughly 44% in April 2025 and retired veCAKE entirely, proving ve(3,3) breaks down when the bribe economy disconnects from real trading demand. On Ethereum, Aero's bribes have to compete with organic liquidity depth it can't match on day one.

So What Would It Take?

There are five conditions for Aero to make the model portable. Each is possible individually:

Aero needs to win Ethereum volume starting with the long-tail.

As shown on Base, ve(3,3) has a real edge in bootstrapping new assets: if the merger coincides with new launches on Ethereum and those projects choose Aero's bribe pipeline over Uniswap's passive model, the flywheel has fuel. The addressable long-tail pool on Ethereum is roughly $30 to $60 billion in annualized volume. Capturing 15 percent of that at a blended 25 bps fee rate produces around $17 million in annualized revenue — that's meaningful growth.

The MetaDEX 03 efficiency gains have to be real.

If the REV Engine actually captures leaked MEV, Aero can offer LPs a better net return than Uniswap without heavy emissions. That would attract liquidity on economic merit rather than subsidies.

Base keeps compounding.

Base's trajectory still matters more than anything Ethereum-related, because Base is already generating the revenue. Ethereum is potential, not realized.

Predictive Allocation has to work.

If veAERO voters can preemptively allocate liquidity to pools based on predicted demand, and earn outsized rewards for being right, that's a capability no order-book exchange or passive AMM can replicate. On Ethereum, where new pairs appear constantly, that could be a real differentiator.

The Relock Rate has to hold on both chains.

On Base it already does, running above 100% with the Aero Fed curbing emissions to match locking demand. On Ethereum, Aerodrome is a price-taker competing with Uniswap, which compresses fee income per veAERO position and could suppress locks. If both chains' Relock weakens simultaneously (which is what a crypto-wide drawdown looks like), supply inflates 3 to 5 percent a year. If it holds at 100%+ on both, supply deflates 3 to 4 percent. That 6 to 9 point gap compounds over multiple years.

Aero has to either generate enough efficiency through MetaDEX 03 that the model works without heavy bribes, or dominate the new-asset bootstrapping niche so convincingly that protocols choose the bribe pipeline over passive AMMs by default.

Running the Numbers

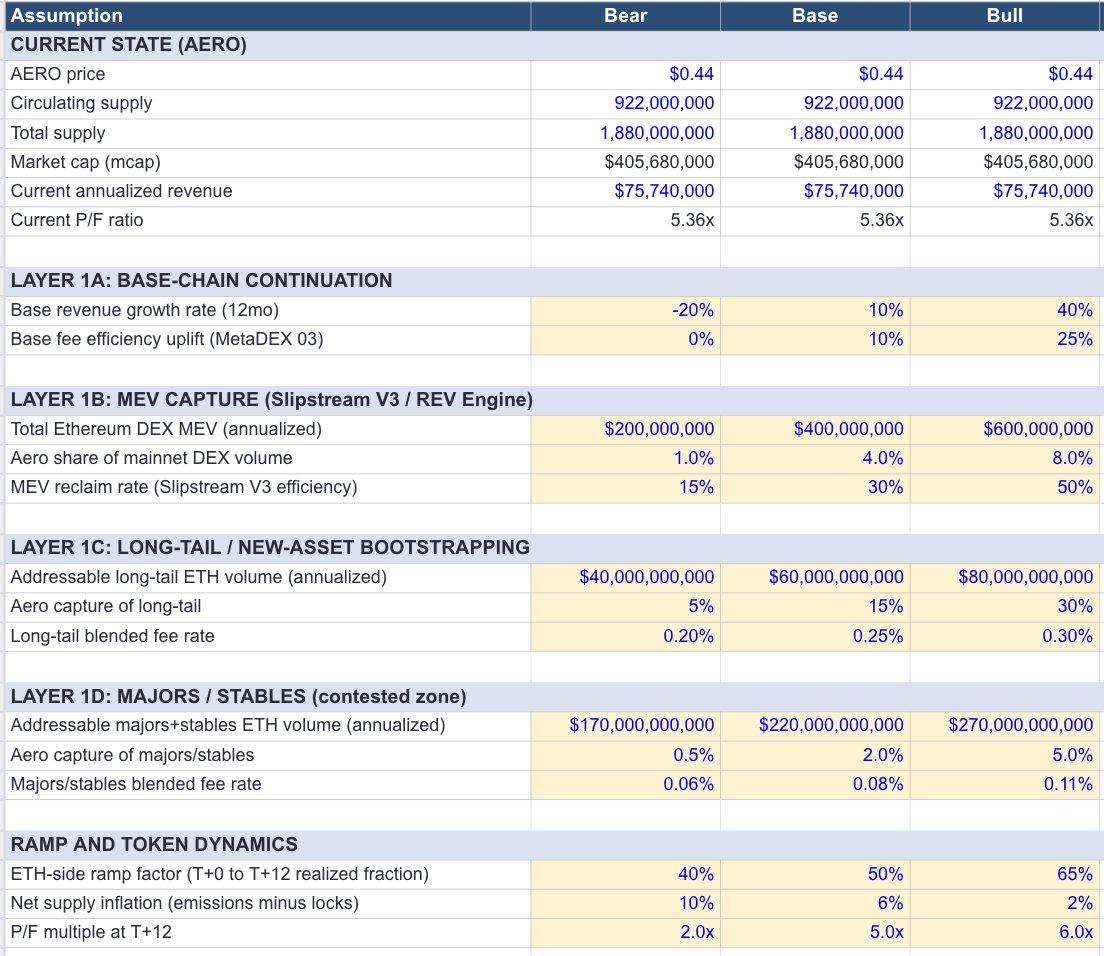

To see which of those two paths the numbers actually support, I built a three-layer model projecting where $AERO lands 12 months after the merger, assuming prices stay level. The layers answer different questions.

Layer 1 decomposes forward revenue into four sources.

- Source A is Base chain continuation: current $75.74 million annualized revenue adjusted for growth and MetaDEX 03 efficiency gains.

- Source B is MEV capture on Ethereum via Slipstream V3, sized as a share of total Ethereum DEX MEV (roughly $400 million annualized in the Base case) scaled by Aero's eventual volume share and a reclaim rate reflecting new efficiency.

- Source C is long-tail bootstrapping, where ve(3,3) has a structural edge against other AMMs.

- Source D is the contested majors and stables zone, where Aero has no particular edge and capture is assumed to be minimal.

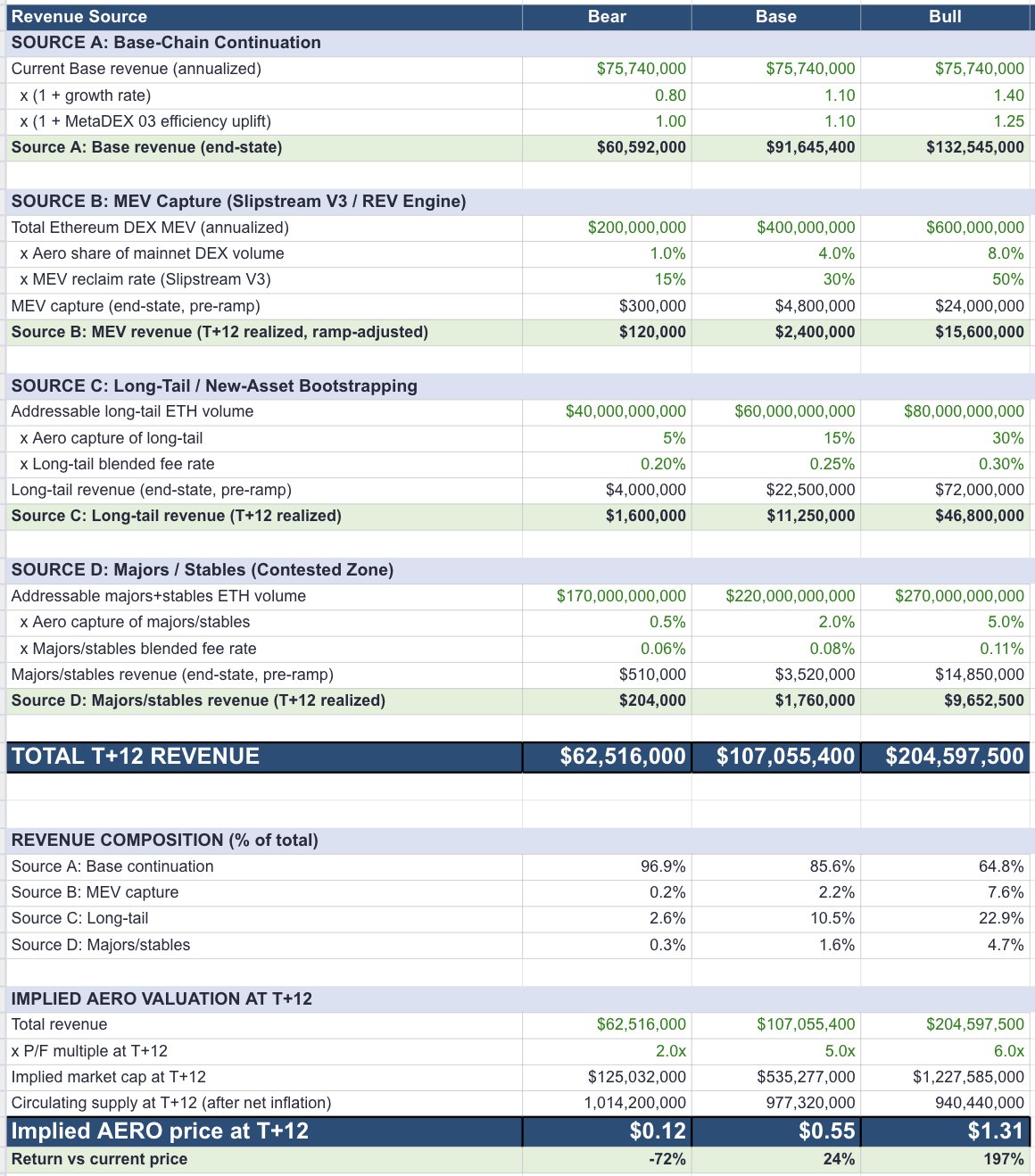

Source A alone is 86% of the total, which is the critical insight. ETH expansion, even in the Base case, adds only 14% to revenue. The story that still matters the most is whether activity on Base keeps compounding — even after Mainnet launch.

Layer 1 outputs:

- Bear case (Base revenue contracts 20%, weak ETH capture across all three ETH sources, 2x P/F multiple): $0.12, or -72% from current.

- Base case (10% Base growth, moderate ETH capture, 5x P/F matching current): $0.55, or +25%.

- Bull case (40% Base growth, strong long-tail capture, full MEV realization, 6x P/F): $1.31, or +197%.

The Base case produces decent return because revenue grows from $75.7M to $107M while the multiple holds flat at the current ~5x. Most of the potential upside lives in the Bull case, where both revenue accelerates and the multiple expands to 6x.

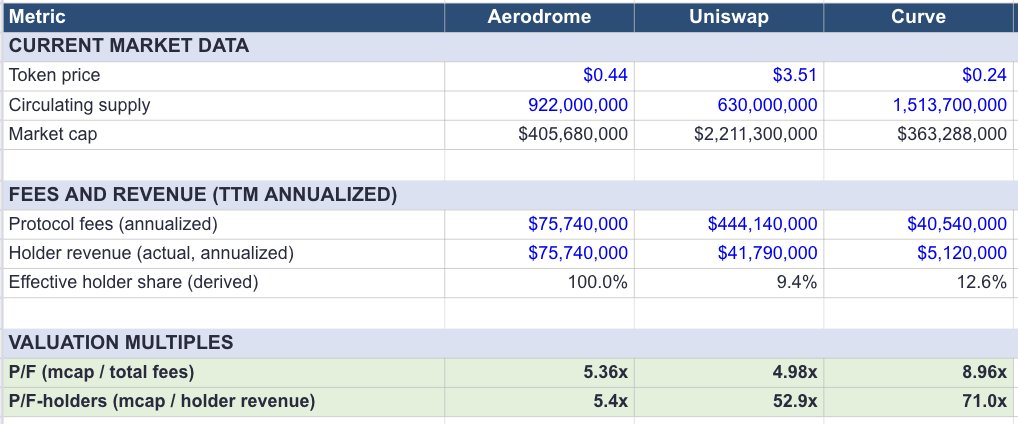

Layer 2 looks at AERO against peers.

On P/F against total fees, Aerodrome trades at 5.4x. Uniswap trades at 5.0x. Curve trades at 9.0x. But the metric that really matters is P/F to token holders: market cap divided by fees that actually flow to the token.

On P/F-holders, Aerodrome trades at the same 5.4x. Uniswap trades at 52.9x because only about 9% of fees currently flow to the UNI burn. Curve trades at 71.0x because its holder revenue is small relative to gross fees, with most of the economics going to LPs and treasury.

The catch is that Uniswap is already closing the gap. As post-UNIfication rollout continues, Uniswap's effective holder share grows from 9% toward its 17% ceiling, compressing its P/F-holders multiple toward Aero's. The window for Aero to trade on its cash-flow advantage won't stay that wide indefinitely.

Layer 3 asks the question from the other direction.

Given a target price, what has to be true?

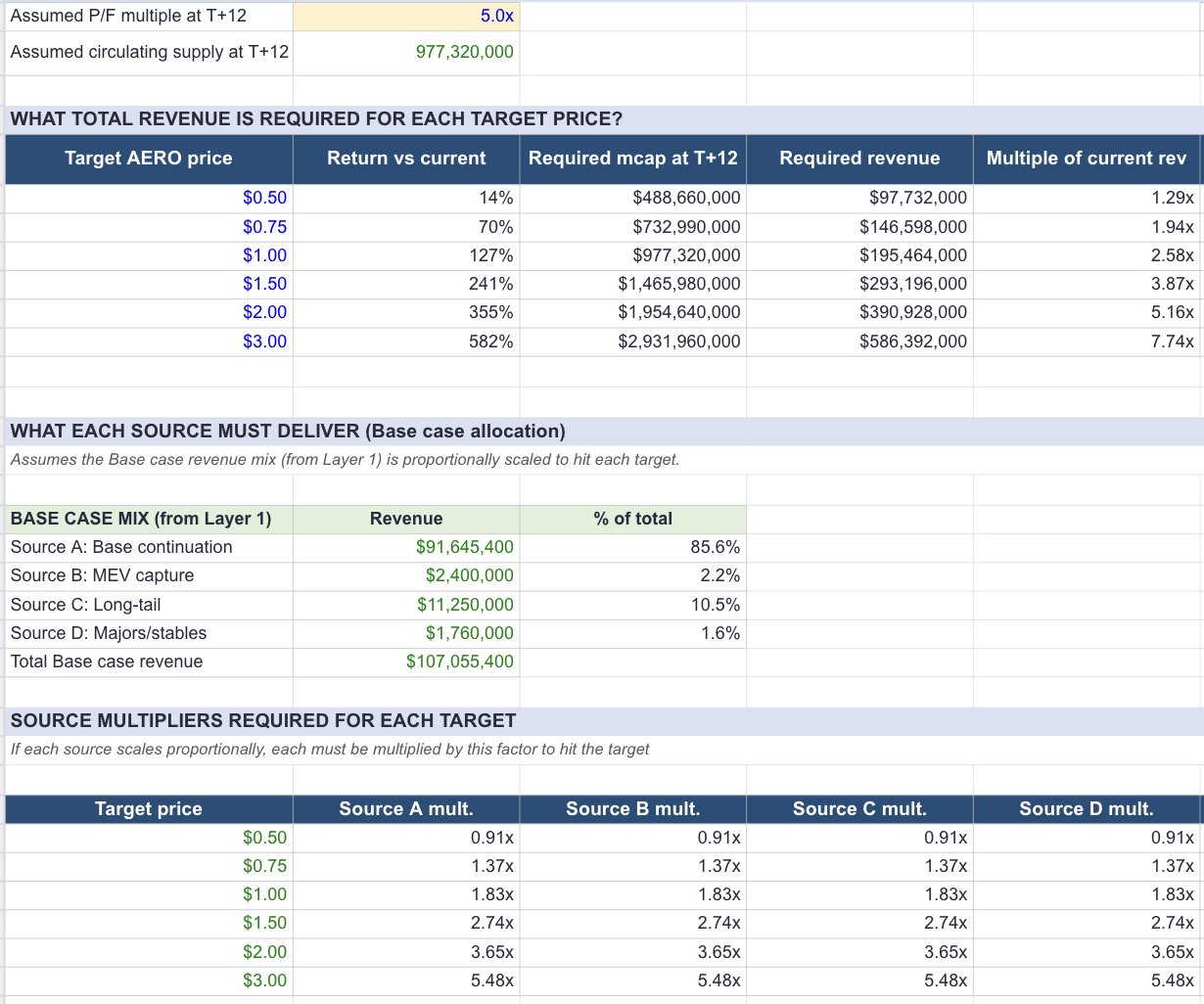

At a 5x P/F multiple and T+12 supply of 977 million tokens:

- $0.75 requires $147 million in total revenue (about 2x current).

- $1.50 requires $293 million (about 4x).

- $3.00 requires $586 million (about 8x).

Layer 3 then decomposes those requirements by source. If you assume uniform scaling then every source has to grow proportionally, but that's not quite realistic. In practice, Source A has a modest ceiling (Base chain depends on macro and the Coinbase flywheel), Source B is capped by Ethereum's MEV pool, Source D is hard to grow against Curve and Uniswap.

Which leaves Source C, long-tail capture on Ethereum, as the only realistic path to large revenue upside.

What this all means. Three things impact Aero's near future. If all three go right, the Bull case might be in range:

- Base chain revenue compounding (this is the foundational revenue source).

- Aero winning the long-tail niche on Ethereum (the growth lever, where meaningful upside lives).

- Aero keeping its 100% tokenholder distribution advantage before Uniswap closes the gap (the rerate).

The path towards a Bear case requires multiple things going wrong at once: Base revenue contraction, weak ETH capture across all three new-revenue sources, and a compressing P/F multiple. Any single lever holding up well keeps outcomes from going meaningfully lower.

What Could Go Wrong

Risks here are ordered by how directly each hits the lock-to-emission equilibrium, which is our core flywheel for the rest to work.

The emission schedule is theoretically infinite. If locking rates decline, dilution wins.

The merger is complex and untested. Cross-chain liquidity unification, embedded MEV capture, and the Ethereum deployment all introduce execution risk the market can't evaluate until the product ships. If Ethereum fails to attract real liquidity demand, emissions there bleed value without the offsetting lock pressure.

Base is a centralized L2. The Base case assumes Base keeps compounding.

Revenue could prove cyclical. Weekly revenue has ranged widely across the past year. If recent periods were softer than the annualization suggests, the real forward run-rate could be lower.

The Base token question remains open. Polymarket odds sit at 40% for a Base token launch by end of 2026. A Base token with its own liquidity incentives could restructure the economics of every protocol on the chain, potentially including Aerodrome's role as the primary emission-direction mechanism.

Operational security. A DNS hijack in November 2025 redirected users to phishing sites and cost over $1 million in losses. Smart contracts weren't touched, but the incident highlights the risk of being the dominant entry point for an entire chain's liquidity.

The Bottom Line

Aerodrome has achieved genuine product-market fit and economic moat on Base: dominant share, top-tier revenue, superior capital efficiency, and a beautiful governance model that has sustained long-dated locking through a brutal drawdown.

But the conditions on Base are what make the flywheel work. When those conditions disappear on Ethereum, the flywheel has to justify itself on efficiency and niche dominance.

What the scenario work makes clear is the range of outcomes. The underlying equity-like quality is Base itself continuing to grow, which it has done steadily since launch. A strong ETH expansion would be the cherry on top.

In any case, the opportunity and the trap live in the same measurement: weekly locks versus weekly emissions. Watch the Relock Rate on Base through 2026, then on Ethereum as the merger deploys.

A sincere thank you to @0xKhmer for his detailed Dune dashboard.

Disclaimer: This article is not financial advice. The views expressed are solely my own and do not reflect those of any other person, firm, or entity.